Strategies for Reducing Auto Insurance Costs

Insurance

|

May 11, 2026

Car insurance premiums have been rising, but that doesn't necessarily mean you have to pay more than necessary. Whether you're renewing an existing policy or shopping for new coverage, there are several proven ways to reduce your insurance costs while maintaining adequate protection. Understanding how insurers determine rates and knowing which discounts and coverage adjustments to consider can help you keep more money in your pocket.

Car insurance premiums have been rising, but that doesn't necessarily mean you have to pay more than necessary. Whether you're renewing an existing policy or shopping for new coverage, there are several proven ways to reduce your insurance costs while maintaining adequate protection. Understanding how insurers determine rates and knowing which discounts and coverage adjustments to consider can help you keep more money in your pocket.

This article explores effective ways to reduce your insurance expenses while ensuring you maintain adequate protection. From evaluating your current policy to taking advantage of discounts and improving your driving habits, we will outline actionable steps that can lead to significant savings. Additionally, we will identify frequent mistakes that drivers make that can unintentionally increase premiums. With the right approach and knowledge, you can take control of your car insurance costs and gain peace of mind on the road. Let’s delve into the best strategies for saving money on car insurance and help you retain more of your hard-earned cash while staying properly protected.

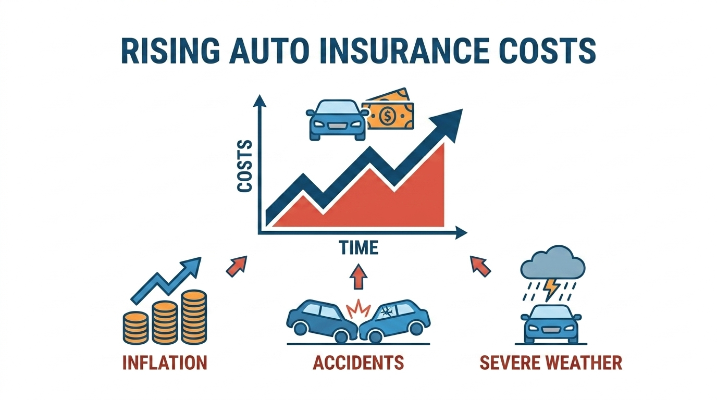

Why Are Auto Insurance Costs Increasing?

Auto insurance premiums have seen a steady rise, and several key factors are driving this trend.

Inflation and Vehicle Repair Costs: Inflation is toughening the economy, influencing the costs related to vehicle repairs and replacements. As the prices for parts and labor climb higher, claims become more expensive, compelling insurers to adjust premiums upward to cover these rising expenses.

Increased Accident and Claim Costs: There has been a noticeable uptick in both the number and severity of car accidents. More collisions lead to more claims, resulting in insurers facing larger payouts. In order to safeguard their profit margins, insurance companies increase premiums to account for these soaring expenses.

Severe Weather and Natural Disasters: Climate change has resulted in an increase in severe weather events, incurring increased damage to vehicles. With the rise in catastrophic occurrences such as floods and hurricanes, insurers are required to account for these risks in their pricing models, consequently elevating premiums.

Changes in Driving Behavior and Risk: The COVID-19 pandemic has significantly altered driving patterns, with many drivers returning to the roads in riskier ways. Recklessness has increased, contributing to heightened perceptions of risk, which, in turn, lead to increased insurance rates.

Personal Factors That Affect Rates: Individual factors like age, location, and claims history play a crucial role in determining insurance costs. Younger drivers, those in high-accident areas, or individuals with multiple claims can face notably higher premiums due to these elevated risk factors.

Understanding these factors can empower consumers to navigate their policies more effectively and explore opportunities for offsetting rising costs.

10 Proven Ways to Save Money on Car Insurance

Car insurance can be overwhelming, but there are straightforward strategies you can adopt to lower your premiums without sacrificing essential coverage. Here are ten proven methods to help you achieve savings on car insurance:

Compare Car Insurance Quotes Regularly

Shopping around and comparing quotes from various insurance providers at least once a year can uncover significant savings. Insurers frequently alter their rates based on competition and your personal circumstances, meaning that a policy that was once the best option may no longer be optimal. Use online comparison tools to streamline the process and discover the best deal tailored to your needs.

Increase Your Deductible

Opting for a higher deductible is a simple way to reduce your monthly premium. A deductible is the amount you pay out of pocket before your insurance coverage kicks in. While this could result in higher upfront costs for claims, if you rarely file claims, the overall savings on your premium may outweigh the risks of increased out-of-pocket expenses.

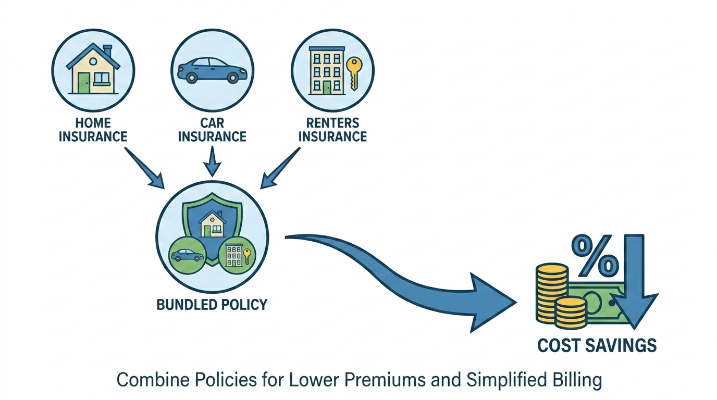

Bundle Insurance Policies

Consider bundling your car insurance with other policies, such as home or renters insurance, from the same provider. Most insurance companies offer discounts for bundling, which can lead to significant annual savings. Additionally, this approach simplifies payments, allowing for a single premium payment rather than multiple, thus improving budget management.

Maintain a Clean Driving Record

Driving safely and avoiding accidents or violations can lead to reduced insurance rates over time. Numerous insurance companies provide safe driver discounts to policyholders who remain accident-free. Participating in defensive driving courses can further enhance your driving skills while also potentially leading to lower premiums.

Improve Your Credit Score

In many jurisdictions, insurance companies factor in credit scores when determining premiums. A stronger credit score can result in reduced rates, making it beneficial to take steps to enhance your credit standing. Paying bills promptly, minimizing debt, and monitoring credit reports can improve your credit score and, consequently, lower your insurance expenses.

Ask About Available Car Insurance Discounts

Don’t hesitate to inquire about any discounts you may qualify for with your insurer. Numerous companies offer discounts for various reasons, including excellent student performance, military service, or membership in certain organizations. Every dollar saved contributes to reducing your overall insurance costs, so be proactive in exploring available savings opportunities.

Take Advantage of Low-Mileage Discounts

If you drive less than the average mileage annually, you might qualify for a low-mileage discount. Many insurers provide lower rates for individuals who do not frequently use their vehicles. This is particularly relevant for remote workers or individuals who utilize public transportation. Be sure to report your low mileage accurately to receive these benefits.

Consider Usage-Based Insurance Programs

Usage-based insurance (UBI) programs track your driving habits through telematics devices installed in your vehicle. If you're a cautious driver who avoids actions like hard braking and rapid acceleration, UBI can provide substantial savings. Numerous insurers offer considerable discounts to encourage safe driving, allowing you to pay based on your actual driving behaviors rather than estimates.

Review Coverage on Older Vehicles

As vehicles depreciate, it may make sense to adjust your coverage. If you possess an older car that holds significantly less value, maintaining comprehensive or collision coverage may no longer be pragmatic. Spend some time evaluating your vehicle’s current worth and adjust your policy to save on unnecessary expenses.

Choose Vehicles With Lower Insurance Costs

When contemplating the purchase of a new vehicle, take insurance costs into consideration as a part of your decision-making process. Certain cars are inherently more costly to insure due to their repair costs, safety ratings, and theft rates. Research and select vehicles noted for lower insurance premiums to save money before finalizing your purchase.

Common Mistakes That Increase Insurance Costs

Buying Coverage Based Only on Price

A prevalent mistake drivers make is selecting insurance solely based on premium costs. While maintaining a budget is key, opting for the cheapest policy can lead to inadequate coverage. For example, a low-priced policy might skimp on essential coverages like comprehensive insurance, which can expose you to high out-of-pocket costs during accidents.

Missing Available Discounts

It’s common for drivers to overlook potential discounts from their insurance providers. Discounts can arise from numerous factors, including bundled policies, good driving habits, or even safety features in your car. Actively seeking these discounts can greatly diminish your expenses, but it demands a proactive approach to ensure you maximize your savings.

Keeping Outdated Coverage

Neglecting to update your insurance coverage after significant life events—such as marriage, moving, or acquiring a new vehicle—can lead to unnecessary expenses. For instance, maintaining a policy that reflects your past situation may result in paying for coverage you no longer require. Regularly reassessing your policies can align them with your current needs and help you avoid overspending.

When Should You Review Your Auto Insurance Policy?

- Annual Policy Renewal

Your auto insurance should be reviewed every year when it renews. This is a critical time to evaluate whether your present coverage meets your current needs and if better rates exist. - Buying or Selling a Vehicle

Whenever you acquire or sell a vehicle, it’s vital to adjust your coverage accordingly. Different cars come with distinct insurance needs—these can significantly affect your premiums and level of protection. - Moving to a New Location

Changing your address can markedly impact your auto insurance rates. Crime rates, local weather conditions, and traffic laws vary by region—this means you should update your policy for optimal coverage.

Expert Tips for Long-Term Insurance Savings

- Review Your Policy Every Year

Regularly revisiting your auto insurance policy allows you to identify areas where you may be overpaying. Look for outdated coverage, unnecessary add-ons, or elements that can be eliminated for savings. - Reevaluate Coverage Needs Regularly

Your insurance needs can shift over time due to circumstances like a new job, relocation, or vehicle changes. Consistently reassessing your coverage helps ensure that you aren’t paying for insurance policies that no longer suit your needs. - Monitor Your Driving Habits

Staying conscious of your driving style can lead to savings. Safe driving may qualify you for discounts, while reckless driving could elevate your rates. Consider tracking your habits and taking defensive driving courses.

Take Charge of Your Auto Insurance Costs

Reducing car insurance expenses is a critical goal for many drivers. Throughout this article, we have explored effective strategies to help you reach that goal without sacrificing essential coverage. Remember, understanding how to save money on car insurance involves a balanced approach—it's crucial to focus not only on affordability but also on ensuring sufficient protection for your needs. Regular assessments of your insurance policies combined with informed choices can significantly enhance your overall financial well-being. Embrace the power of knowledge and stay proactive in optimizing your insurance needs while ensuring peace of mind on the road.

Was this helpful? Share your thoughts